EE details new pricing structure

EE again sets the tone and is the first UK telco to abolish % and CPI pricing.

This represents another fascinating move by EE to take a lead in moving away from the inflation-linked approach (CPI + 3.9%), for its 24-month contracts.

Interestingly, BT Consumer has included inflation-linked mid-contract price rises in its customer terms & conditions for over 10 years (initially using RPI for EE mobile, introducing CPI for BT from 2019, then CPI+ 3.9% from Sept 2020 for all three brands).

To be clear, CPI +3.9% pricing continues until the end of March 2024, and the move towards a pounds and pence model will kick in for new and regrading customers from early Summer (ahead of the Ofcom timeline). Therefore, it will likely take some time for the new terms to reach across the base.

In terms of pricing, the mobile change will be from £1.50 (for example SIMO; likely more for handset customers) and broadband will be £3. While this seems to be a guide, expect to see full details closer to launch. Unsurprisingly, there will be no changes for the lowest income customers on Social Tariffs.

All of this is in response to Ofcom’s review of inflation-linked mid-contract price rises released in mid-December, 2023. It took a pretty strong stance indicating a ban on such activity based upon the fact that users’ contracts do not provide sufficient certainty about the prices they will pay. There is currently a consultation on this proposed new requirement until 13 February 2024, with plans to publish a final decision in spring 2024.

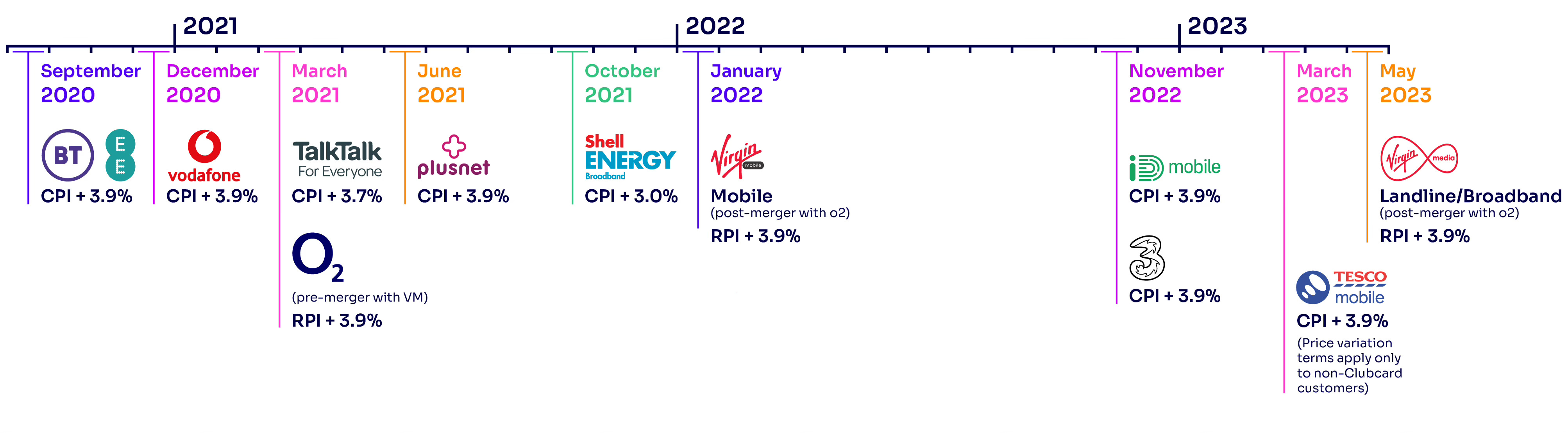

Figure: Introduction of inflation-linked price variation terms, including an additional fixed percentage

Source: Ofcom

While Ofcom’s remit is to protect customers, there appears to be some genuine concern regarding how these rises are communicated; more so during a contract. Telcos must be clear upfront. It is becoming harder for customers to look for a new deal as it is hard to predict future inflation rates. This, in turn, means that consumers are unable to know the total cost of their contract when they sign up.

This is something that will wrangle on given the financial challenges everyone is facing. Ultimately, this is something for Government, as general consumer law does not prevent companies from increasing their prices during the contract period.

All telcos are struggling to generate new forms of revenue. Margins are being squeezed, and there is a distinct lack of revenue growth beyond growth increases. This is further compounded by the rollout of next-generation connectivity, including fiber and 5G, to satisfy users' insatiable appetite for data.

While Ofcom’s move might appear to be a major blow for the UK telcos, the direction of travel for pricing is clear. With a clear trend towards higher pricing, here lies an opportunity for telcos to be somewhat creative with how services are bundled. Some (and more so the challenger brands) may seek to be disruptive. Other converged players may look to package converged services akin to a more-for-more approach, as well as offer more hyper-personalized tariffs as seen in other markets, such as Verizon in the US with myPlan.

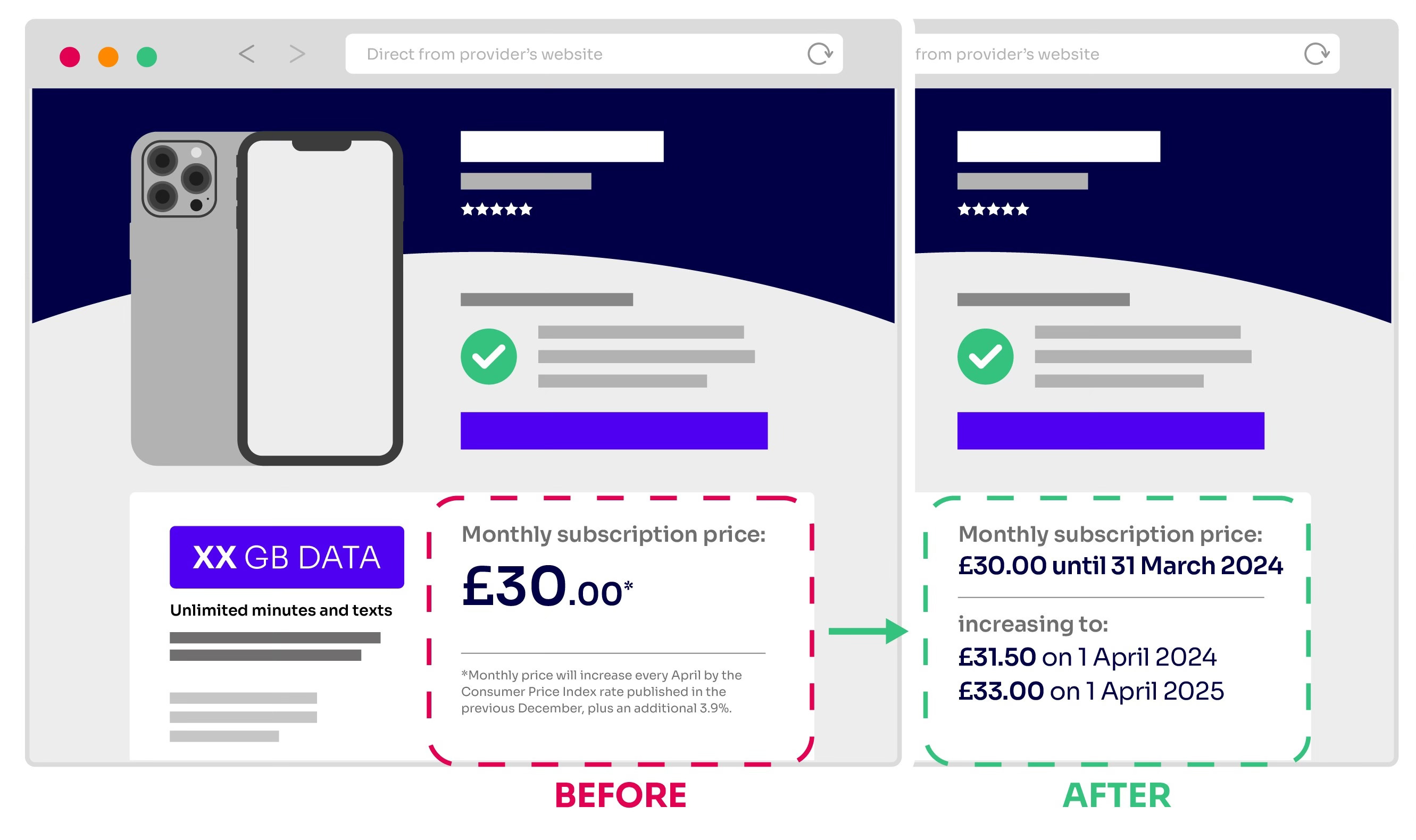

The approach set out by the new EE consumer unit for BT is consistent with Ofcom’s original thinking (see below).

Figure: An example of how the £/p requirement would apply

Source: Ofcom

With all of the brands under the EE consumer unit adopting this new approach, it does fit nicely into the overall new vision for the consumer segment as it transitions the base towards a more subscription-based model. Now expect other UK providers to follow suit with their own models.